SPACs, also known as blank check companies, are not a new concept; they have been around for more than 30 years. However, 2020 was a record year for SPACs in the U.S., and 2021 is continuing on that path. Per SPACInsider (spacinsider.com/stats/), SPAC IPOs in the U.S. raised almost twice as much in 2020 as they raised in the previous 10 years combined. SPAC gross proceeds for the first four months of 2021 alone have exceeded that of calendar year 2020. Through April 2021, SPACs have raised more than $100 billion in gross proceeds, compared to $83.3 billion in 2020, and $13.6 billion in 2019.

With the frenzy around SPACs, the fear of missing out may be accompanied by a fear of not knowing (about SPACs), but being too afraid to ask. This blog provides the basics: what is a SPAC, how do SPACs work and why are they so popular.

What is a SPAC, in Brief?

A SPAC, or Special Purpose Acquisition Company, provides an alternative route—versus the traditional IPO market—for privately held companies to go public.

A SPAC is a company with no commercial operations. Its sole purpose is to raise capital through an initial public offering to merge with or acquire one or more existing private companies.

Capital raised by the SPAC is kept in an interest-bearing trust account. SPACs typically have about two years to make an acquisition, which must be approved by shareholders. If they are unable to complete a deal, money is returned to investors.

Once a SPAC is approved, the private company goes public with a new ticker; the SPAC no longer exists.

Terms to Know

| SPAC | A Special Purpose Acquisition Company. The sole purpose of a SPAC is to raise capital through an initial public offering (IPO) to merge with or acquire one or more existing private companies. A SPAC is a company with no commercial operations. |

| Sponsor | The entity that forms the SPAC and funds the offering expenses in exchange for SPAC founder shares, commonly 20%. |

| Acquisition target | The privately held company that is being considered by the SPAC Sponsor and must be approved by SPAC shareholders. |

| Business combination | Once the acquisition target has been identified and vetted, a business combination is announced then voted upon by SPAC shareholders. |

| Blank check company | SPACs are often referred to as blank check companies because SPAC IPOs seek to raise capital to purchase or merge with a yet-to-be-determined private company. |

| De-SPACing | Once the business combination is complete, the SPAC no longer exists. The process is called “de-SPACing”. |

| SPAC units | SPAC units are offered at the time of the IPO. A unit consists of a share of common stock and a (portion of a) warrant. Beginning approximately 50 days after IPO, the common stock and warrants may be bought and sold separately. |

| Warrant | A warrant gives the holder the right to purchase a specific number of shares of common stock at a specific price during a specific time. |

| Trust account | Cash raised by a SPAC is held in a trust account, and generally invested in U.S. government securities or money market securities, until a business is acquired, or the SPAC is liquidated without an acquisition and the money is returned to investors. |

How Does a SPAC Work?

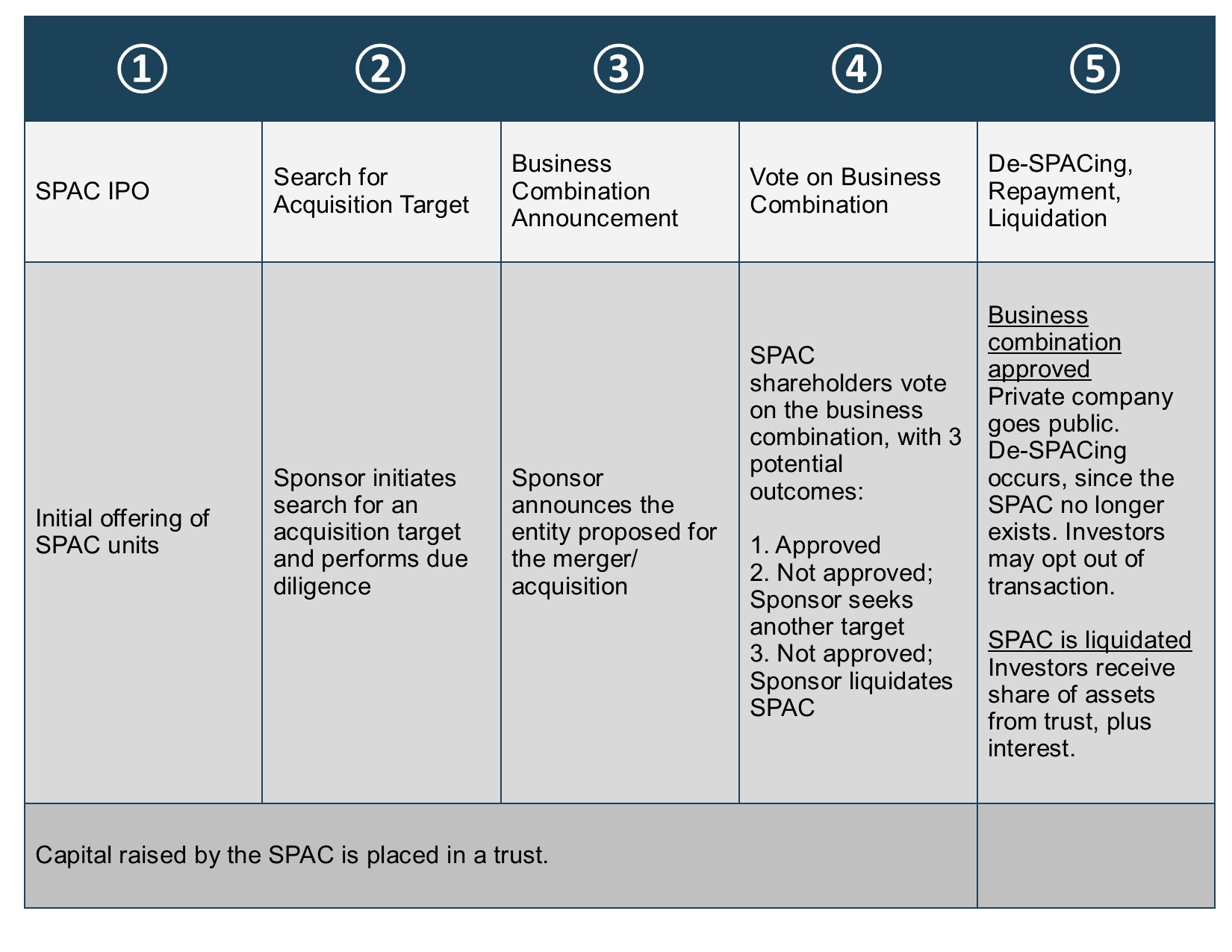

We describe and illustrate the SPAC process in 5 steps.

Step 1: SPAC IPO.

The Sponsor forms the SPAC and funds the operating expenses. The initial offering of SPAC units takes place through an IPO. SPAC units shares are generally issued for $10/share, inclusive of a common share and warrant (or portion of a warrant). After the IPO, SPAC units trade in the open market. Approximately 50 days post-IPO, common shares and warrants may be bought and sold separately in the open market.

Capital raised by the SPAC is placed in an interest-bearing trust account until a deal is solidified or the SPAC is dissolved.

Step 2: Search for acquisition target.

The Sponsor seeks out and evaluates acquisition targets.

Step 3: Business combination announcement.

The Sponsor announces a business combination following initial due diligence on the acquisition target company.

Step 4: Vote on business combination.

SPAC shareholders typically vote on the business combination. There are three potential outcomes from this phase. One: Shareholders approve and there follows a review and commenting period by the SEC. Two: Shareholders withhold approval, and the Sponsor seeks another acquisition target. Three: Shareholders withhold approval, and the Sponsor liquidates the trust to redeem shares sold in the IPO.

Note that acquisition targets are usually valued at 2-4 times the value of the IPO proceeds. The additional funding needed to finance a merger or acquisition is usually made through debt financing or PIPE (private investment in public equity) deals offered to institutional investors before the merger or acquisition is announced to the public.

Step 5: De-SPACing, repayment, liquidation.

Once the business combination is complete, the SPAC no longer exists. This is referred to as the de-SPACing process. The newly established public company trades under a new ticker symbol. Investors who don’t wish to invest in the new company may redeem their shares. If the SPAC doesn’t make an acquisition during the stated period, the SPAC dissolves, investment money is returned to the investors and the warrants expire worthless.

Timeline: 18-24 months from IPO to Business Combination

Popularity of SPACs

The popularity of SPACs can be viewed through the lens of three parties: investors, acquisition companies and Sponsors.

Benefits to investors. SPACs give investors access to private-equity-like investments through experienced managers (the SPAC Sponsors).

Downside mitigation. Net proceeds from the IPO are placed into a trust account that accumulates interest.

Investors are guaranteed to get their money back if they do not approve the merger/acquisition within the stated time frame. Further, investors have a right to redeem their shares prior to a merger/acquisition.

Upside potential. Investors have potential upside through stock appreciation and warrant value.

Benefits to acquisition targets. SPACs provide numerous benefits for acquisition companies.

Faster, cheaper. SPACs allow private companies to go public through a process that is typically faster and cheaper than the traditional IPO route, which could take up to two years and cost 10% of IPO proceeds. SPACs often require three to five months until IPO and the costs are lower.

Control. The pandemic has caused the traditional IPO market to be more volatile and uncertain, leading companies to pull their offerings. A merger with a SPAC gives a private company more control and certainty, at a lower cost. Target companies lock in a stock price with the SPAC Sponsor, protecting against market uncertainty.

Access. SPACs provide access to experienced managers and a wider range of capital.

Benefits to Sponsors. SPACs provide attractive economics for Sponsors if a target is secured and shareholders approve. Sponsors typically reap a 20% equity promote (through founder shares) and private placement warrants. Further, SPACs allow Sponsors to focus on one material acquisition.

Final Thoughts

Ultimus LeverPoint offers full accounting and bookkeeping services for SPAC and Sponsors as they are launching the SPAC, during the life of the SPAC, and prior to the de-SPACing process. Services include: 1) preparation of financial statements and footnotes for SEC filing requirements; 2) monthly bookkeeping of the SPAC; 3) maintenance of the shareholder registry; and 4) Treasury services. By leveraging Ultimus staff, Sponsors are relieved of SPAC-related management duties, while accessing industry best practices and accounting platforms. Learn more here, Ultimus LeverPoint SPAC Services.