Launching an Exchange-Traded Fund: Is it Right for Your Firm?

Since the introduction of the first ETFs in the early 1990s, they have garnered a sizeable portion of the market for pooled investment products. In recent years, nearly as many ETFs have closed as have launched. What do those disparate facts mean for asset managers?

There is no doubt ETFs can have a place in investor’s portfolios and as part of an asset manager’s product lineup. Investors have come to expect that ETFs will have lower expense ratios than comparable mutual funds, and indeed at high asset levels ETFs can be less expensive to operate. Meeting customer expectations for lower cost can cause a margin squeeze for an adviser sponsoring a smaller ETF. Likewise, there are advantages and disadvantages for ETFs compared to mutual funds when it comes to distribution. Some platforms allow trading of any exchange-listed product, which could broaden distribution possibilities, but wholesaling ETFs can be more challenging than mutual funds, and many retirement platforms do not support offering ETFs.

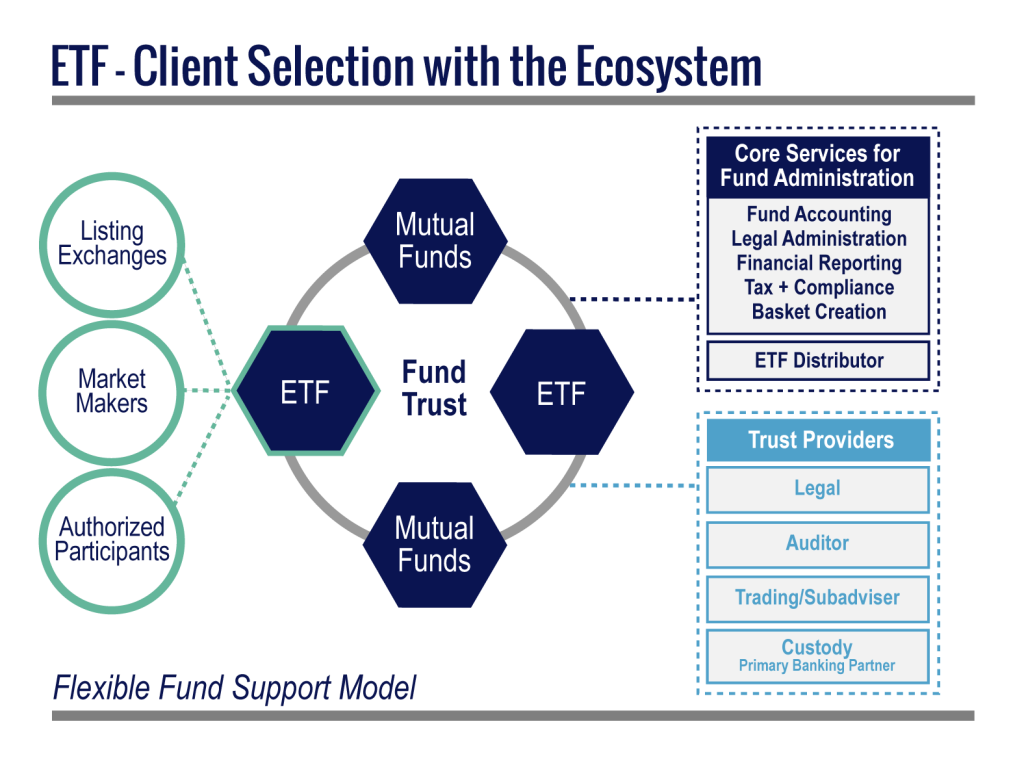

An ETF launch may seem complex, but Ultimus’ extensive list of partnerships throughout the ETF ecosystem will help you strategize and properly manage all of the moving parts involved for a successful fund launch, watch this explainer video about the ETF ecosystem to learn more. There are no shortcuts to learning about the ETF ecosystem. With Ultimus’ deep product knowledge and industry connections, we assist asset managers to help them understand the various parts of the ETF ecosystem, their role in the ecosystem, and the intricacies involved in a comprehensive and operationally efficient fund launch, including proactive introductions to the necessary parties involved and project management of the ETF launch.

Ultimus supports all aspects of launching and operating ETFs and our professionals have the expertise to help you evaluate whether offering an ETF is right for your firm. Contact us today to learn more.