Since the first Exchange-traded fund (ETF) premiered in 1993, ETFs have experienced tremendous growth as an accessible investment vehicle for both retail and institutional investors. By 2021, ETFs in the U.S. represented 7.2 trillion U.S. dollars.¹

What is behind the ongoing—and increasing—popularity of ETFs? We believe the growth is attributable to the benefits obtained by ETF issuers and investors alike, as well as to strategy and structural innovations.

Know Before You Go

This blog will cover things to know about ETFs before you consider a launch:

- How ETFs compare to mutual funds

- Behind-the-scenes: ETF mechanics

- ETF structural choices

- The SEC’s role in innovation

Exchange-Traded Funds vs. Mutual Funds

ETFs are similar in several ways to mutual funds. Both pool investor capital. Both invest in a broad array of strategies. Both offer passively managed funds designed to track a specific index, and actively managed funds composed of securities uniquely selected by an investment manager.

But ETFs have certain advantages over mutual funds:

- Exchange Traded and Intraday Pricing. In keeping with its name, ETFs trade on stock exchanges (NYSE, Cboe, and NASDAQ), while mutual funds must be purchased through other channels, such as brokerage firms. Since ETFs trade on exchanges, they trade throughout the day, offering greater liquidity. Mutual funds, on the other hand, trade only at their daily closing price.

- Fees. ETFs typically are less expensive than mutual funds.

- Tax Efficiency. ETFs are generally more tax efficient than mutual funds. In a traditional mutual fund, portfolio managers sell portfolio holdings to meet shareholder liquidations or to rebalance the portfolio. The sales of these securities can generate taxable capital gains that are passed on to shareholders.

In the ETF structure, securities don’t always need to be sold to meet investor redemptions. Rather, ETF shares can trade directly between investors. When redemptions exceed the inventory on the secondary market, baskets of assets that approximate a pro rata slice of

the ETF are redeemed in kind, and the fund is not required to distribute capital gains from those transactions to the remaining shareholders.

ETFs started primarily as passively managed funds that track to specific indexes, however over the past two years, actively managed ETFs have seen considerable growth in assets and the number of new funds coming to market.

ETFs generally offer transparency to their underlying holdings on a daily basis. Some ETFs use shielding mechanism to show a representative portfolio but mask the true portfolio composition.

ETFs are generally not offered in 401(k) channels for a number of reasons. The infrastructure for 401(k)’s was developed prior to ETFs being widely available and recordkeeping systems used in these plans were not designed to deal with products that can trade throughout the day. ETFs are also not traded in fractional shares, making small incremental investments difficult. Also, since 401(k)s are tax deferred, they do not benefit from the tax efficiency that ETFs offer.

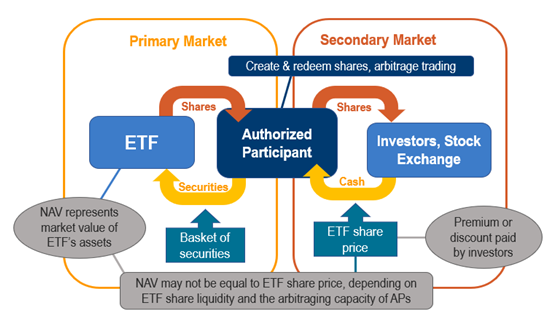

Behind-the-Scenes: The Mechanics

The number of shares outstanding in an ETF structure fluctuates daily due to the ongoing issuance of new shares and redemption of existing shares.

The ability of ETFs to issue and redeem shares continuously helps keep the current market price in line with the net asset value of the underlying securities in the portfolio.

The create/redeem process for ETF shares is handled between the ETF sponsor and an authorized participant (AP).

The diagram below illustrates the key players and share flow for ETFs.

ETF Structures

The ETF structure is most commonly set up as a registered investment company (RIC) that is professionally managed by a registered investment adviser and regulated by the Investment Company Act of 1940. As a RIC, an ETF is governed by a board with independent trustees who are responsible for: i) approving contracts, ii) ensuring that the fund designs and implements comprehensive compliance policies and procedures, and iii) providing continual oversight of fund operations on behalf of shareholders.

Most ETFs are classified as open-end funds, similar to mutual funds. Nonetheless structural variety abounds:

Open-End Funds. Most open-end ETFs are structured as RICs, explained above. In addition, open-end ETF funds are priced daily and allow an investor to buy and sell shares of the fund any day that trading is open. The funds are required to distribute income and capital gains directly to shareholders.

Unit Investment Trusts (UIT). Some of the first exchange-traded funds were formed as unit investment trusts. A unit investment trust generally has a fixed portfolio of securities and a fixed term. UITs, like open-end funds, are governed by the Investment Company Act of 1940. There are, however, a few distinctions between the two; UITs do not have boards of directors or investment advisers.

Exchange-Traded Grantor Trusts. Grantor trusts are most often used to form ETFs that hold physical assets, such as precious metals. These products cannot receive income and are required to hold a specific amount of underlying assets. Investors in these funds are viewed as direct holders of the underlying asset.

Exchange-Traded Notes (ETNs). Exchange-traded notes trade like ETFs on a stock exchange, however ETNs are unsecured debt securities that generally follow an index. ETNs promise to pay an amount equal to the return of the index less the management fee. ETNs have inherent credit risk as they are considered debt instruments, not assets.

The SEC’s Role in Innovation²

Exemptive Relief. In September 2019, the SEC passed Rule 6c-11 to, “…facilitate greater competition and innovation in the ETF marketplace, leading to more choice for investors.” The adoption was intended to bring ETFs to market more quickly without the time or expense of applying for individual exemptive relief. Prior to approval of the Rule, the SEC had issued more than 300 exemptive orders allowing ETFs to operate under the Investment Company Act. One condition of the Rule is to disclose daily holdings of the ETF.

The exemptive relief provided by Rule 6c-11 applies only to open-end funds.

Semi-Transparent / Non-Transparent ETFs. Back in May 2019, the SEC granted exemptive relief under the Investment Company Act of 1940 on a number of applications to allow investment advisors to bring ETFs to market that do not provide daily transparency of the portfolio composition. These actively managed ETFs, also known as non-transparent or semi-transparent ETFs, allow active portfolio managers to reap the benefits of the ETF structure while hiding or masking the underlying holdings to protect their strategy.

Precidian Investments, New York Stock Exchange, Fidelity Investments and Blue Tractor were among some of the advisors that received exemptive relief.

ETF Investment Strategies |

| ETFs come in a multitude of strategies, covering domestic and foreign markets.

Bond ETFs. Bond, or fixed income, ETFs provide exposure to one or a mixture of bonds, including U.S. Treasuries, corporate, municipal, international, and high-yield bonds. Stock ETFs. Stock, or equity, ETFs hold a portfolio of individual stocks; many are passively managed and track a specific index. Sector and Industry ETFs. These ETFs are designed to provide exposure to a specific sector, such as Health Care, or industry, such as Biotechnology. Commodity ETFs. Commodity ETFs provide exposure to commodities, such as gold. These ETFs commonly invest in derivatives that track the underlying value of the commodity rather than directly owning the underlying assets. ETFs that do hold physical commodities like gold are typically set up as Grantor Trusts. Style ETFs. Style ETFs are designed to follow a specific investment style or market capitalization focus, like large-cap value or small-cap growth. Thematic ETFs. These ETFs offer portfolios based on particular themes such as technology advances and social trends. Currency ETFs. Currency ETFs can be used to hedge a portfolio against currency risk and may invest in a single currency or many different currencies. |

Conclusion

ETFs provide investment managers an opportunity to expand their product offering and attract additional investors. For investors, ETFs offer an opportunity to invest in a relatively low-cost product that offers tax efficiency, transparency, and liquidity. ETFs continue to gain significant investment flows as the types of investment strategies broaden.

Investment managers seeking to add ETFs to their product mix should consider working with an experienced fund administrator to help evaluate ETF structures and provide guidance on launching an ETF.

²https://www.sec.gov/news/press-release/2019-190

15052255 5/20/2022